Behind the number: Real cost of your CIBIL score

Your CIBIL score impacts loan approvals and interest rates significantly. Timely repayments and checking your credit report can help maintain a healthy score

- Jul 23, 2025,

- Updated Jul 23, 2025, 12:10 PM IST

In India’s rapidly digitising economy, one metric has emerged as a powerful determinant of financial eligibility: the CIBIL score. Once a footnote in the fine print of a loan document, this three-digit number—ranging from 300 to 900—has evolved into a critical filter in accessing credit. Whether it’s securing a home loan, applying for a credit card, or even renting an apartment in metros, the CIBIL score now holds significant sway over who gets financial opportunities and who doesn’t.

Initially intended as a measure to promote responsible lending, the CIBIL score is today functioning as a financial gateway. While it has served banks and NBFCs well in managing risk, the system is now being scrutinised for excluding those who fall outside the formal credit grid.

Cash-Dependent Citizens: Invisible in the Credit Matrix

India’s working population is mostly comprised of wage labourers, small vendors and informal sector workers whose primary mode of transaction is cash. For such individuals, the formal financial engagement means the absence of a credit history; despite them being financially responsible, their transactions remain undocumented in the modern financial language. This results in them being in a situation of being credit-invisible. Being in this situation will move them away from taking loans for housing, education or emergencies still a nightmare. All this is due to the absence of a CIBIL score and not because they are risky borrowers.

The Importance of CIBIL in Today's Financial Landscape

Over the last decade, the credit landscape of India has undergone a dramatic shift because of the development in smartphones, fintech applications, and the most promising one was the introduction of digital payment systems like UPI easier access to credit, especially for urban youth. On a day-to-day basis, people have started exploiting the options of Buy Now, Pay Later (BNPL) schemes, app-based credit lines, and microloans as their means of everyday purchases. Along with the ease of access, it has increased surveillance as well. As a result, the financial institutions, including the traditional and digital now consider CIBIL score as a proxy for creditworthiness. While the systems still face everyday inconsistencies, such as payment delays due to technical glitches or unreported loan closures.

EMI, BNPL, and the Score Slippage

A major contributor to credit score fluctuations today lies in EMI plans and BNPL schemes. These services, although designed to encourage consumption by deferring payments, can quickly become traps. A single missed or delayed EMI can trigger a negative report to credit bureaus, pushing the score downward.

Another under-discussed issue is the closure of long-standing credit cards. Users, in an attempt to reduce debt exposure, may shut down older cards—only to see their credit score dip due to a shortened credit history. Such intricacies are rarely communicated clearly, leaving borrowers exposed to avoidable score drops.

Navigating Credit Challenges: The Gen Z Perspective

India’s Gen Z is the first generation to grow up entirely in a digital financial environment. With access to instant credit, they are also navigating a complex system that penalises seemingly minor decisions. Multiple credit card applications can label them as “credit hungry,” while treating BNPL dues as harmless can backfire when missed payments surface in their credit reports. This disconnect between the behaviour and the system expectations is often witnessed during significant life events, such as applying for an education loan or housing loan, by which the damage will be done, and the path to correction will be long and opaque.

Factors Shaping the Score

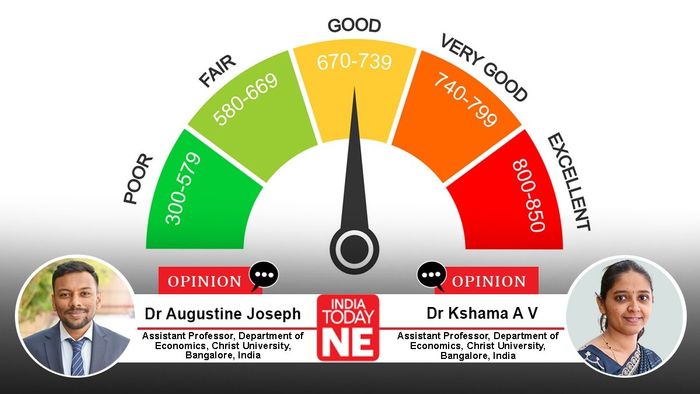

A CIBIL score is based on key factors like repayment history, credit utilisation, credit age, credit mix, and the number of credit enquiries. Timely payments boost the score, while delays hurt it. On the other hand, using over 30-40% of your credit limit or applying for multiple loans frequently can impact your score negatively. A mix of secured and unsecured loans, along with a long credit history, is considered a positive. Having said all of this, many first-time borrowers are unaware of the factors and the ways to manage or improve their credit scores.

Strategies for Building Your Score

For beginners, the best way to begin is to kick-start with building a positive credit history by using secured credit cards or through small digital loans. Start reviewing your credit report annually to catch any errors and avoid multiple credit applications in a short period. On-time payment of EMIs and credit card dues, while keeping the credit card usage below 30% and holding on to older credit cards, will boost the individual's score. All these will end up in a good CIBIL score, which is achievable with consistency and financial awareness.

Efforts to Raise Awareness

When we speak about credit literacy, it is still limited to urban or digital-savvy segments. While some private platforms and banks offer free credit score tracking through applications, financial influencers explain the credit dynamics through social media, which again is focused on people living in metros. The Government-led efforts, such as Financial Literacy Week, organised by RBI and inclusion of modules in skill development programs (like PMKVY), will bridge the awareness gap, but despite the efforts, outreach is still relatively minor given the scale of the challenge faced.

Policy Interventions: Toward Broader Inclusion

As India is considered to be an emerging economy, the financial system also evolves in the process, taking into consideration policies aimed at bridging the gap between the credit-visible and the credit-invisible. As a regulating agency, RBI can take the key role by promoting the use of transactions such as rent, utility, and mobile payments as alternatives to strengthen the credit profiling. Steps should be taken to encourage digital transactions among cash-based earners. A system should be in place to solve credit report errors, and encourage and integrate vocational education and financial literacy, since schooling can collectively help in building a more inclusive and transparent credit ecosystem.

Humanising the Numbers

In recent times, CIBIL has played a crucial role in encouraging people to follow credit discipline and aid in minimising lending risks. In a diverse and most populous country like India, where most of the people work in the informal economy, leading to widespread cash transactions, a metric like CIBIL would be skewed, as it excludes the majority of the population who contribute to the economy. The process of credit assessment should evolve by considering the varied realities of borrowers, offering flexibility and fair access to those without an official record of credit. Still, a question persists: should financial opportunity only belong to those already familiar with the system, or can it be extended to those ready to participate and grow?