GST’s Next Decade Must Belong to Simplicity, Trust and Technology

When the Goods and Services Tax was launched at the stroke of midnight on July 1, 2017, it marked a rare moment of fiscal consensus in a deeply diverse federal democracy. The venue itself, the Central Hall of the old Parliament building, gave the reform a historic character. It was not simply the introduction of another tax. It was the beginning of a new indirect tax architecture for India.

- Jun 30, 2026,

- Updated Jun 30, 2026, 3:39 PM IST

When the Goods and Services Tax was launched at the stroke of midnight on July 1, 2017, it marked a rare moment of fiscal consensus in a deeply diverse federal democracy. The venue itself, the Central Hall of the old Parliament building, gave the reform a historic character. It was not simply the introduction of another tax. It was the beginning of a new indirect tax architecture for India.

GST replaced a complex structure of central and state taxes, including excise duty, service tax, value added tax, central sales tax, entertainment tax, octroi and several cesses. For decades, this layered system had created cascading taxation, fragmented markets and administrative uncertainty. Businesses operating across states often faced multiple levies, check posts, documentation burdens and classification disputes. Consumers ultimately bore much of this inefficiency in the form of higher costs.

The promise of GST was therefore both economic and institutional. It sought to create a common national market, reduce tax cascading, improve compliance, broaden the tax base and strengthen public revenues. It also required the Centre and states to share taxation authority through the GST Council, making it one of India’s most important experiments in cooperative federalism.

Nearly a decade later, the broad direction of the reform is clear. GST has survived its difficult birth. It has expanded India’s tax base, improved revenue visibility, encouraged formalisation and made indirect taxation more transparent than before. But the success of the next decade will not be determined merely by collection figures. It will be determined by whether GST can become simpler, fairer and more predictable for ordinary taxpayers.

This is the real challenge now. GST 2.0 represents the next stage of India’s indirect tax reform. Its central purpose is to make the tax system simpler, more transparent and more responsive to the needs of business. The focus is now on rationalising rates, reducing compliance burdens through deeper digitalisation, improving the input tax credit mechanism and strengthening ease of doing business. By streamlining procedures and reducing classification disputes, GST 2.0 can improve tax administration, protect revenue and support sustained economic growth.

In agriculture too, GST 2.0 can bring practical gains by simplifying the tax treatment of farm inputs, irrigation equipment, storage, transportation and agri machinery. While many basic agricultural products remain outside the GST net, a more rational and predictable system can reduce hidden costs across the supply chain, improve market access and support food processing and allied rural enterprises. If implemented carefully, these reforms can ease cost pressures on farmers and strengthen the broader rural economy.

The first phase of GST was about implementation. The second phase was about stabilisation. The third phase must be about maturity.

At the time of launch, India had about 66.5 lakh registered taxpayers under GST. By 2026, this number had increased to around 1.6 crore. This expansion reflects a deeper process of formalisation in the economy. More businesses are now within the tax net. More transactions leave a digital trail. More enterprises are connected to invoice systems, return filing platforms and input tax credit mechanisms.

This is an important achievement. Formalisation is not only about collecting more taxes. It improves access to credit, strengthens business records, reduces informal cash-based operations and helps policymakers understand economic activity more accurately. For a large and complex economy like India, such visibility is valuable.

Revenue collections also show the growing strength of the system. Average monthly GST collections have risen sharply since the early years of implementation. Gross GST revenue has crossed the Rs 20 lakh crore mark annually, reflecting stronger compliance, wider coverage, improved economic activity and better enforcement tools. The regular improvement in collections has also eased some of the early concerns of states that feared revenue losses after surrendering several independent tax powers.

But revenue growth, while important, cannot be the only measure of success. A tax system must also be judged by the experience of those who comply with it.

For large companies, GST compliance can be managed through dedicated finance teams, consultants and technology systems. For small businesses, the experience is very different. A delayed refund can disrupt working capital. A mismatch in input tax credit can create financial pressure. A notice from the department can cause uncertainty. A classification dispute can consume time and resources that a small enterprise can ill afford. This is why the next decade of GST must belong to simplicity.

The original GST structure had four main slabs of 5, 12, 18 and 28 per cent, along with a compensation cess on luxury, sin and demerit goods. Such a structure may have been politically necessary during the initial transition, but it also created complications. Products often became trapped in classification disputes. Businesses had to interpret rate schedules carefully. Tax administrators had room for differing views. Litigation and confusion were inevitable.

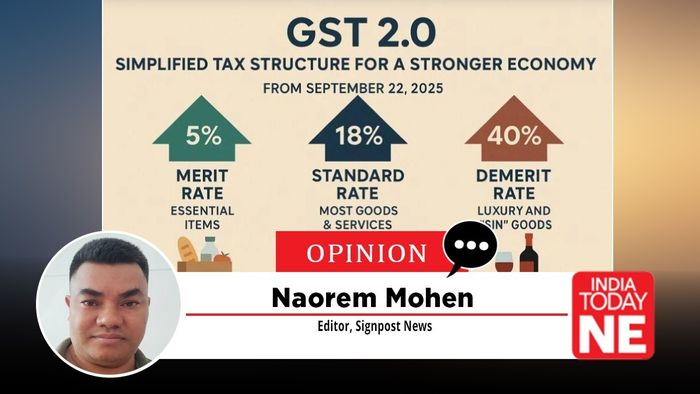

The move towards a rationalised rate structure is therefore a significant step. Beginning September 22, 2025, India moved to a next generation GST framework with two principal slabs of 5 per cent and 18 per cent, while retaining a separate 40 per cent rate for luxury and demerit goods. Essential goods and services were placed under the lower rate, while standard goods and services attracted the 18 per cent rate.

This rationalisation was long overdue. A simpler rate structure helps businesses comply better. It reduces classification disputes. It allows consumers to understand the tax burden more easily. It also improves the credibility of the system because taxation becomes less dependent on technical interpretation.

Simplicity, however, cannot be limited to rates. It must extend to returns, refunds, audits, notices, appeals and input tax credit rules. If the rate structure becomes simpler but the compliance process remains complicated, the reform will remain incomplete.

The government’s growing use of artificial intelligence, data analytics and integrated digital platforms can play an important role in this new phase. GST has already become one of India’s largest digital governance systems. E-invoicing, e-way bills, online return filing and data based scrutiny have improved the ability of the administration to track transactions and detect evasion.

The next step is deeper integration of GST, income tax and customs databases. Such integration can improve risk assessment, reduce manual verification, identify suspicious patterns and accelerate legitimate refunds. It can also help detect fake invoicing, circular trading, shell entities and wrongful input tax credit claims.

This is necessary. Tax evasion weakens public revenue and creates unfair competition for honest businesses. A system that allows fake invoices and fraudulent credit claims punishes those who follow the law. Technology driven enforcement is therefore not merely an administrative preference. It is essential for protecting the integrity of the tax system.

But technology must be used with care. Artificial intelligence cannot become an invisible instrument of harassment. Data flags must not automatically be treated as proof of wrongdoing. Risk assessment should guide inquiry, not replace judgment. Taxpayers must have access to clear reasons, timely responses and fair appeal mechanisms. A modern tax system must be strict against evasion but respectful towards compliance.

This distinction is crucial. The honest taxpayer should not feel that every interaction with the department begins from suspicion. Compliance must be encouraged through certainty, speed and fairness. Enforcement must be targeted, evidence based and proportionate. Trust is therefore as important as technology.

GST rests on two forms of trust. The first is trust between the taxpayer and the tax administration. The second is trust between the Centre and the states. Both must be protected.

The taxpayer must trust that the system will not change unpredictably, that refunds will not be delayed without reason, that notices will be meaningful, and that disputes will be resolved in a reasonable time. Businesses plan investment, pricing and supply chains based on tax certainty. Frequent changes, unclear classifications and procedural delays create avoidable friction.

The federal dimension is equally important. GST was possible because states agreed to pool substantial taxation powers into a shared framework. The GST Council became the institutional mechanism through which the Centre and states negotiated rates, exemptions, procedures and structural changes. This arrangement has generally worked, despite political differences.

That must continue. Rate rationalisation, inclusion of new goods, changes in compensation arrangements and major compliance reforms must be carried out through transparent consultation. States must feel that their revenue concerns are respected. The Centre must ensure that the spirit of cooperative federalism remains intact. GST cannot become a centralised tax in practice while remaining federal in form. One unfinished issue illustrates this tension clearly: petroleum.

Crude oil, petrol, diesel, aviation turbine fuel and natural gas are constitutionally within the GST framework, but their actual inclusion depends on a decision by the GST Council. So far, petroleum products remain outside GST because both the Centre and states derive substantial revenue from them. States, in particular, remain cautious about any move that could reduce their fiscal space.

This caution is understandable. But keeping petroleum outside GST also has costs. Fuel is a major input for transport, logistics, manufacturing and aviation. When such products remain outside the input tax credit chain, costs get embedded into the economy. This weakens the completeness of GST as a value added tax system.

Bringing petroleum into GST will require careful preparation. It cannot be done casually. It will need a credible compensation mechanism, realistic rates and political consensus. But it must remain part of the long term reform agenda. A comprehensive GST cannot indefinitely exclude such a major segment of the economy.

Another unfinished area is dispute resolution. Any large tax system will generate disputes, especially in a country with India’s economic diversity. But the quality of a tax system is reflected in how quickly and fairly those disputes are resolved. Delayed adjudication locks capital, creates uncertainty and increases litigation costs. This is particularly harmful for small and medium enterprises.

The operationalisation and strengthening of GST appellate mechanisms must therefore be treated as a priority. Taxpayers need a credible forum where disputes can be resolved without excessive delay. A faster appeal process will also improve departmental discipline because poor quality orders are more likely to be corrected.

Industry feedback suggests that GST is now broadly accepted. Businesses recognise the benefits of digitisation, rate rationalisation and a unified national market. But acceptance should not be mistaken for complete satisfaction. Many enterprises still face problems related to input tax credit mismatches, refund delays, notices, audits and procedural complexity.

This is where the next decade must be different from the first.

The first decade required patience because India was building a new system. The next decade will require discipline because India must improve that system. The tolerance for confusion will naturally decline. Taxpayers who have adapted to GST will expect stability. Businesses that have invested in compliance infrastructure will expect predictability. States that surrendered tax powers will expect fairness. Consumers will expect rate reductions to translate into actual price benefits. The central objective should be clear: make GST easier for those who comply and harder for those who evade.

This requires administrative design, not slogans. Refund systems must become faster. Return filing must become more intuitive. Small taxpayers must receive simpler compliance options. Notices must be precise and reasoned. Classification disputes must be reduced through clearer guidance. Artificial intelligence tools must be transparent and accountable. The GST Council must continue to function as a serious federal institution.

The reform also needs better communication. Taxpayers should not learn about important changes only through consultants, circulars or last minute clarifications. A system of this scale needs clear public explanation, multilingual guidance and predictable timelines. Compliance improves when rules are understood.

GST has already changed India’s fiscal structure. It has made taxation more digital, more visible and more integrated. It has helped build a wider tax base and stronger revenue system. It has also shown that major fiscal reform is possible in India when political negotiation and administrative technology work together.

But the work is not complete. The next decade of GST must not be judged by ambition alone. It must be judged by the quality of implementation. A mature GST should reduce disputes, not multiply them. It should support enterprise, not intimidate it. It should use technology to improve fairness, not merely to intensify scrutiny. It should strengthen federal cooperation, not weaken it.

India does not need GST to become louder. It needs GST to become better. At ten, GST stands at an important point. The difficult question of survival has been answered. The more demanding question of refinement remains. If the coming decade belongs to simplicity, trust and technology, GST can move from being a major tax reform to becoming a mature instrument of economic governance.

That is the real promise of GST’s next decade! GST’s first decade proved that India could implement a national indirect tax. Its next decade must prove that India can make it simple, fair and predictable.